The Georgia First-Time Homebuyer Guide: An Overview

Buying your first home in Georgia can feel overwhelming. After two decades as a real estate closing attorney, I’ve seen hundreds of buyers navigate this…

Buying your first home in Georgia can feel overwhelming. After two decades as a real estate closing attorney, I’ve seen hundreds of buyers navigate this journey. The great news is that Georgia offers some of the best programs in the country to help new homeowners.

From the Georgia Dream Homeownership Program to federal loan options, more help is available than you might think. This Georgia first-time homebuyer guide offers essential steps and programs to simplify your path to homeownership.

I. Getting Ready to Buy: Your Financial Game Plan

Your financial health determines everything in the homebuying process. I’ve seen buyers with high incomes get denied because they didn’t prepare. I’ve also seen buyers with modest salaries succeed because they took the time to get their finances in order.

Assessing Your Credit Score and Report

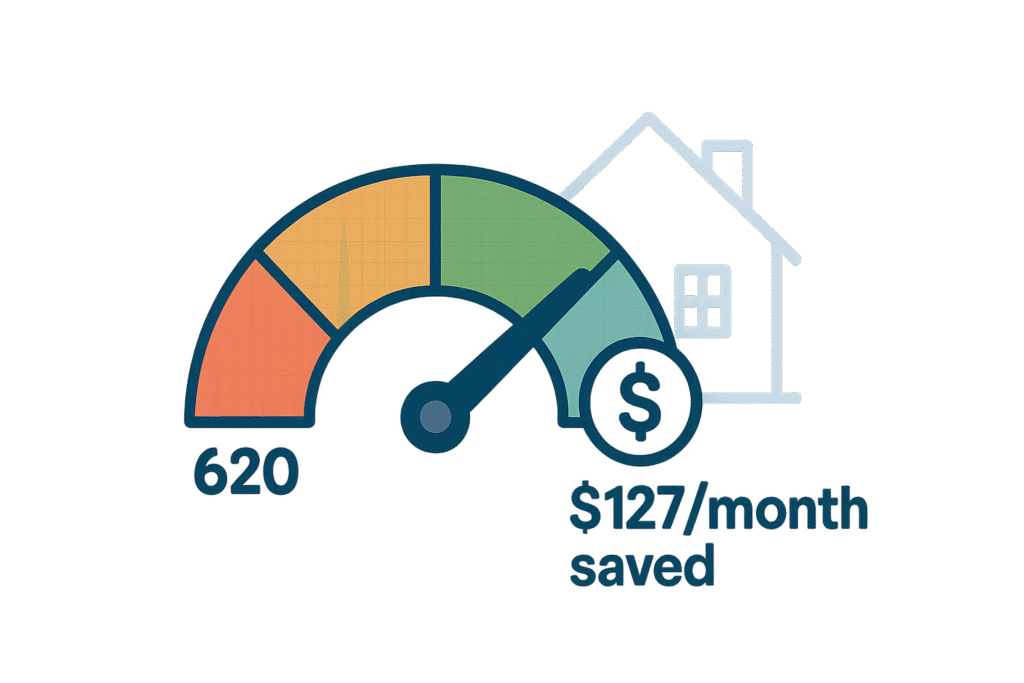

A higher credit score can save you thousands of dollars over the life of your loan. A score of 740 can get you a much better interest rate than a score of 620.

- Check your credit report from all three major bureaus at least six months before you start house hunting.

- Look for errors, old accounts, and potential red flags.

- Dispute any inaccurate information right away.

To improve your score:

- Pay down credit card balances to below 30% utilization.

- Keep old credit cards open, as they help with your credit history length.

- Pay all of your bills on time for at least six months.

One buyer I worked with raised their score 80 points in four months. That one change saved them $127 every month on their mortgage payment.

Calculating Your Debt-to-Income Ratio (DTI)

Mortgage lenders care about your DTI more than almost anything else. It shows whether you can afford the monthly payments for your new home in addition to your current bills.

The DTI formula is simple:

Total monthly debt payments ÷ Gross monthly income = DTI percentage

Most lenders prefer a DTI below 43% for conventional loans. FHA loans may allow for a slightly higher ratio.

Include these in your debt calculation:

- Credit card minimum payments

- Auto loans

- Student loans

- Personal loans

- Child support or alimony

Do not include living expenses like utilities or groceries in this calculation.

Saving for a Down Payment and Closing Costs

The price of the house is not your only expense. Many first-time homebuyers forget to budget for closing costs, moving expenses, and immediate repairs.

Your total costs usually include:

- Down payment, which varies by loan type

- Closing costs (2-5% of the home’s price)

- Home inspection ($300-$500)

- Appraisal fee ($400-$600)

- Moving expenses

- Immediate repairs or improvements

| Loan Type | Down Payment | Mortgage Insurance | Key Eligibility |

|---|---|---|---|

| FHA | 3.5% | Required | Credit score ≥ 580 |

| VA | 0% | None | Military service, COE |

| USDA | 0% | Required | Rural areas, income limits |

| Conventional | 3-20% | PMI if <20% equity | Follows Fannie Mae/Freddie Mac |

Ways to save for these costs:

- Set up automatic transfers to a dedicated savings account.

- Use windfalls like tax refunds or bonuses for your down payment.

- Ask family members about gift funds, but make sure to get proper documentation.

II. Finding Assistance: Key Georgia First-Time Homebuyer Programs

Georgia offers several programs to make homeownership more accessible. It’s smart to explore all your options.

The Georgia Dream Homeownership Program

This is the state’s main assistance program for first-time buyers. Run by the Georgia Department of Community Affairs (DCA), it offers affordable mortgage financing and down payment assistance.

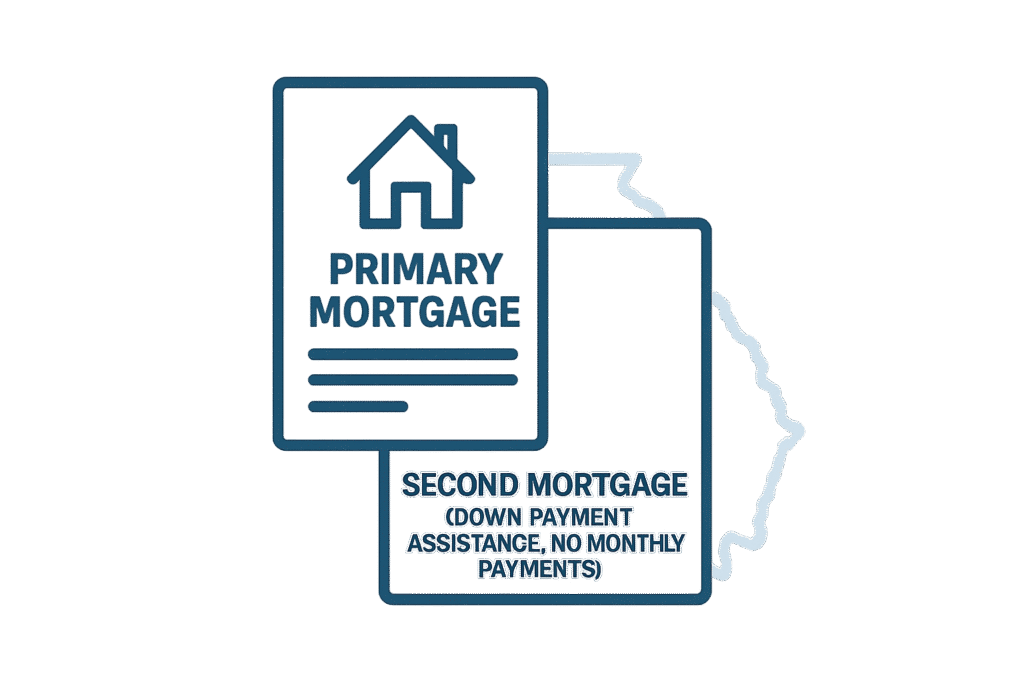

This program gives you two loans:

- Your primary mortgage.

- A second mortgage for down payment and closing cost assistance.

The second mortgage has no monthly payments.

Eligibility for the Georgia Dream Program

The program defines “first-time homebuyer” as someone who has not owned a primary home in the past three years. This also includes divorced individuals or single parents who only owned a home with a former spouse.

Other criteria include:

- Income limits vary by location and household size.

- Purchase price limits apply to homes purchased.

These limits change every year. Always confirm the current criteria with a participating lender.

Other Key Loans and Programs

Government-backed loans are a great option for many buyers. They often offer more flexible terms than conventional loans.

FHA Loans

FHA loans are backed by the Federal Housing Administration. They are popular with first-time buyers.

FHA loan benefits:

- Lower down payment requirements, starting at 3.5%

- More flexible credit standards

- Sellers can contribute up to 6% toward closing costs

FHA loan considerations:

- You must pay mortgage insurance premiums.

- Property must meet FHA standards.

VA Loans

Active military members and veterans can access some of the best mortgage terms available through VA loans.

VA loan advantages:

- No down payment required

- No private mortgage insurance

- More flexible qualification standards

VA loan requirements:

- You must have qualifying military service.

- You must obtain a Certificate of Eligibility.

I’ve helped many clients with VA loans. They offer great terms for those who qualify.

USDA Loans

These loans are for moderate-income buyers in eligible rural and some suburban areas.

USDA loan features:

- Zero down payment option

- Below-market interest rates

- Income limits apply

Check USDA eligibility maps online. You might find that many areas outside major cities like Atlanta, Augusta, and Savannah qualify.

Conventional Loans

Conventional mortgages are not backed by the government. Instead, they follow guidelines set by Fannie Mae or Freddie Mac.

Conventional loan benefits:

- No upfront mortgage insurance

- Private Mortgage Insurance (PMI) can be removed once you reach 20% equity.

- More property types are available.

Local and County-Specific Programs

Don’t forget to look for local assistance. The Fulton County Homeownership Program, for example, provides additional down payment help. Additionally, Invest Atlanta offers down payment assistance programs for first-time homebuyers purchasing within the City of Atlanta, such as the Home Atlanta Program, which provides up to $20,000 in forgivable loans.

Research these options:

- County housing authorities

- City-specific first-time buyer programs

- Employer-assisted housing programs

- Non-profit organization assistance

Many of these programs can be used with state and federal assistance.

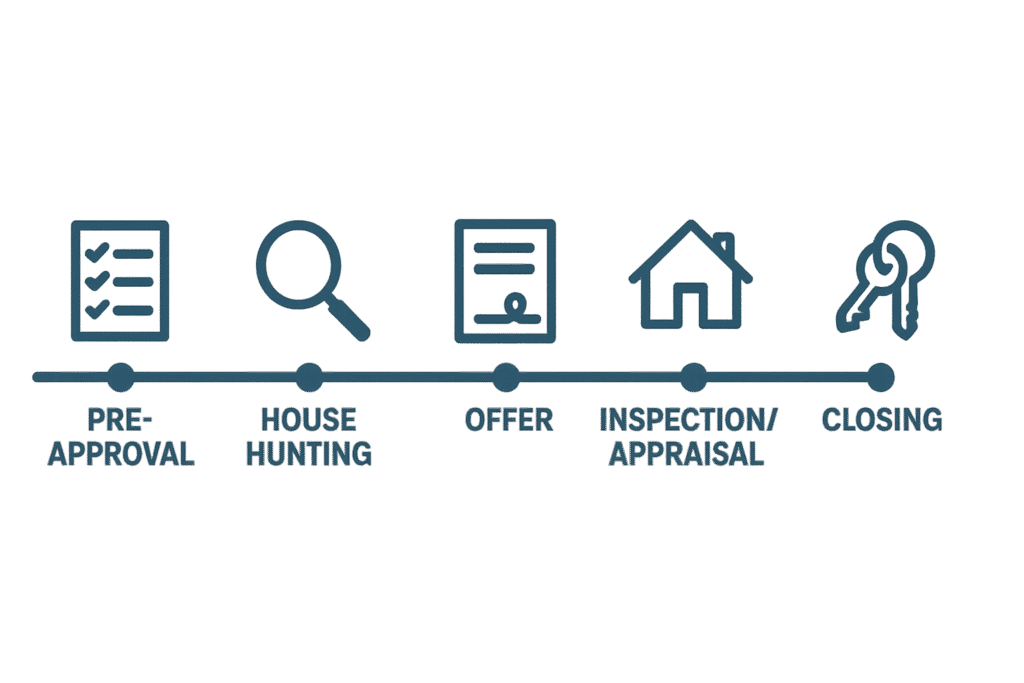

III. Your Homebuying Journey: A Step-by-Step Guide

The homebuying process involves a series of steps, from finding your team to getting the keys.

Building Your Team

You need a great team to guide you. The two most important people are your real estate agent and your mortgage lender.

Finding the Right Real Estate Agent

A local agent is your advocate. They know neighborhoods, schools, and market trends you can’t find online.

Look for an agent who:

- Specializes in first-time buyers.

- Knows your target neighborhoods well.

- Responds quickly to your questions.

- Understands the available assistance programs.

Ask them these questions during an interview:

- How many first-time buyers did you help last year?

- How do you help buyers in competitive markets?

- Can you recommend trusted inspectors?

Partnering with a Qualified Mortgage Lender

This is where you get pre-approved for your loan. A pre-approval letter tells sellers that you are a serious buyer because a lender has verified your ability to get financing.

Organize these documents for your lender:

- Recent pay stubs

- Tax returns from the past two years

- Bank statements from the last few months

- Employment verification letter

- Asset documentation, like your 401k or savings

The Hunt and the Offer

This is the fun part. But it’s also where you can make emotional mistakes.

House Hunting and Open Houses

Before you start looking, make a list of your “must-haves” and “nice-to-haves.”

Must-haves include things like:

- Number of bedrooms and bathrooms.

- School district requirements.

- Commute distance limits.

Nice-to-haves might include:

- A specific architectural style.

- A large yard.

- Upgraded finishes or appliances.

During open houses, check things like cell phone reception and look for signs of needed repairs.

Making an Offer

Your offer is more than just a price. It also includes terms, timing, and contingencies.

Strong offers include:

- A competitive price based on recent sales.

- A pre-approval letter from your lender.

- An adequate earnest money deposit.

- Appropriate contingencies for inspection and financing.

Your agent should research recent sales before suggesting an offer strategy. Strategies that work in rural Georgia might not work in metro Atlanta.

From Contract to Keys: The Closing Process

The final steps are all about protecting your investment and finalizing the deal.

The Home Inspection and Appraisal

These steps protect you and satisfy your lender.

A home inspection covers things like:

- Electrical, plumbing, and HVAC systems.

- Roof and structural components.

- Windows, doors, and insulation.

An appraisal confirms the home’s value. It protects you from overpaying in an inflated market.

Finalizing Your Loan and Closing

Three days before closing, you will get your Closing Disclosure. This document lists all the final costs and terms of your loan. Review it carefully.

At the closing table, you will:

- Sign all the loan documents and the deed.

- Get your keys and garage door openers.

- Receive copies of important documents.

Closings usually take a little over an hour.

IV. Post-Purchase: Life as a Homeowner

Your responsibilities do not end once you get the keys.

Budgeting for the Long Term

Your monthly payments include more than just the loan. You also need to budget for:

- Property taxes, which vary by county.

- Homeowner’s insurance.

- Utilities, which are often higher than in an apartment.

- Regular maintenance (1-3% of the home’s value each year).

- Emergency repairs.

Start an emergency fund just for home repairs. Major systems do not break at convenient times.

Building Equity

Homeownership builds wealth through equity and appreciation. Each monthly payment increases your ownership stake.

Equity builds through:

- Principal reduction with each payment.

- Property value appreciation over time.

- Home improvements that add value.

Focus on making a home you will enjoy living in. Building wealth happens over years, not months.

V. FAQ: Common Questions from Georgia First-Time Homebuyers

How long does the homebuying process take?

Typically, it takes 30-60 days from the time a seller accepts your offer until closing. Factors that can affect this timeline include:

- The type of loan you have.

- The results of the inspection.

- Any issues with the property title.

Can I get a home loan with bad credit?

Yes, but your options will be limited. FHA loans accept credit scores as low as 580 with a 3.5% down payment.

If your credit is a concern, consider these strategies:

- Work with an experienced lender.

- Try to improve your credit before applying.

- Have a larger down payment.

What are some of the biggest mistakes a first-time homebuyer can make?

The biggest mistake is not preparing properly. Here are some of the most common and expensive mistakes I have seen:

- Shopping for homes before getting a pre-approval.

- Not budgeting for closing costs and other expenses.

- Not researching neighborhoods.

- Taking on new debt while you are trying to get a mortgage.

- Draining all of your savings for the down payment.

Taking the time to educate yourself and working with experienced professionals can save you a lot of time, money, and stress.

VI. Final Thoughts on the Georgia First-Time Homebuyer Guide

Buying your first home in Georgia takes preparation and patience. The Georgia first-time homebuyer guide is an excellent place to start. Each step, from understanding your finances to exploring assistance programs, brings you closer to owning a home.

The state offers excellent opportunities for first-time buyers. Take advantage of programs like the Georgia Dream Homeownership Program, as well as federal options like FHA and VA loans.

Your next steps are simple:

- Check your credit report.

- Research assistance programs.

- Get pre-approved with a qualified mortgage lender.

- Find a local real estate agent.

- Start house hunting within your budget.

Work with a participating lender who understands the programs in the Georgia first-time homebuyer guide. They can help you navigate the process. Your dream of homeownership in Georgia is closer than you think.